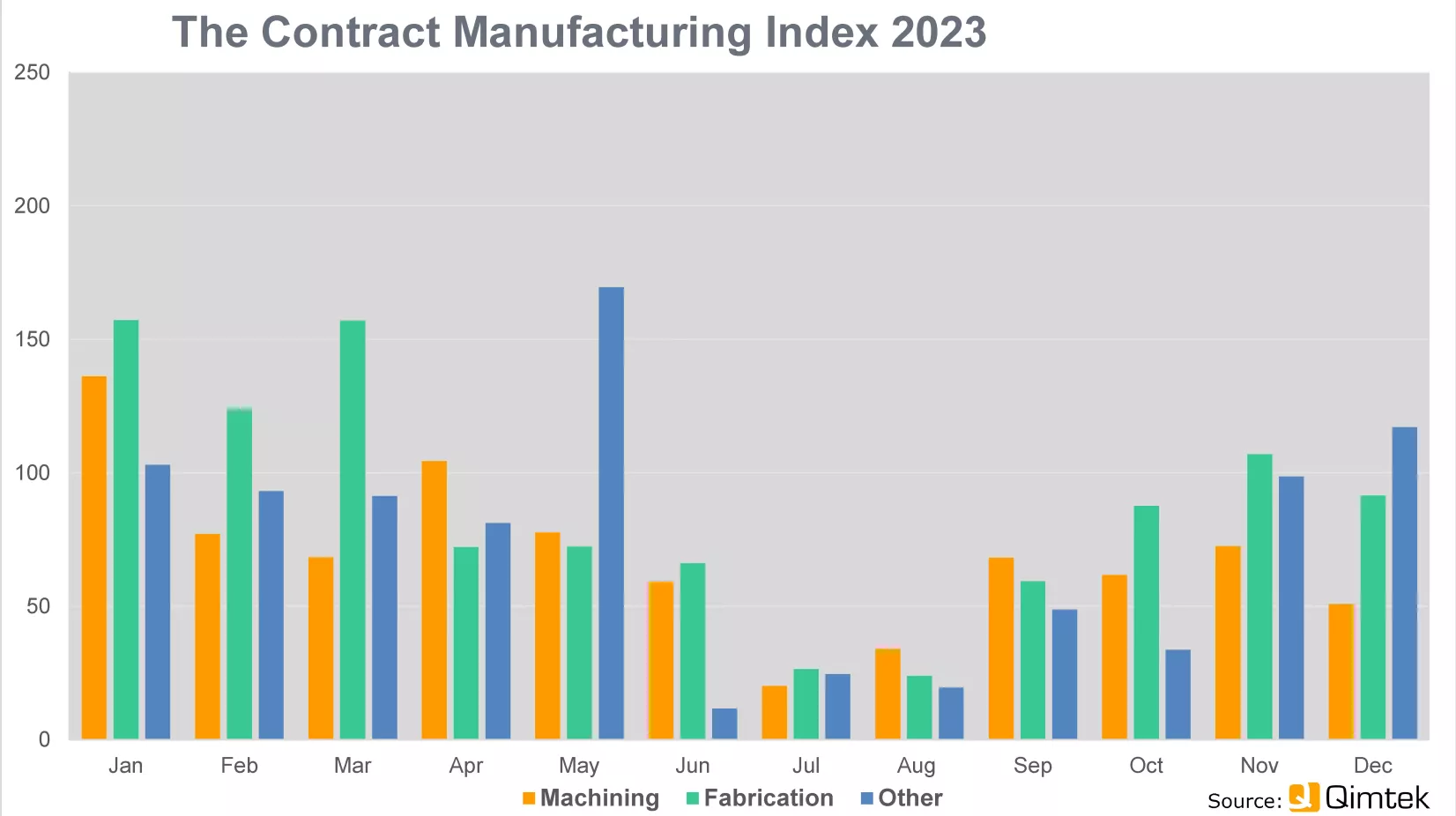

The latest Contract Manufacturing Index (CMI) shows that the UK market for subcontract manufacturing ended the year on a strong positive note after a difficult twelve months.

Performance during the year was driven down by buyers putting new projects on hold and focusing on reducing stock in response to uncertain demand. It reached an all-time low in August.

The rebound in the fourth quarter was impressive, with the market up 106% compared to the previous three months as purchasing organisations unlocked budgets and started to place new work with suppliers.

Overall the market ended the year 7.5% higher than at the end of 2022.

The market got off to a strong start in January but quickly tailed off to hit new lows in July and August. The recovery started in September and carried on picking up momentum for the rest of the year.

On a process-by-process basis, fabrication was the strongest area of the market – up 160% on the previous quarter and 12% on the previous year. Growth in machining was less strong but still significant – up 51% on the previous quarter but just 2.4% up on the previous year. Other processes including moulding and electronic were up by just 0.5% year-on-year.

The largest single sector throughout the year was Industrial Machinery, with Food & Beverage second and Electronics third.

Qimtek is now also tracking average lead time, which stayed consistent throughout the year at 22 days.

Commenting on the figures, Qimtek owner Karl Wigart said: “The main reason that 2024 was a slow year was that a lot of new projects were being kept on hold and buyers were concentrating on using up their existing stock.

“It seems as if the optimistic view we had at the end of the third quarter was justified and Q4 did see a good rebound of activity among both buyers and suppliers. Buyers suddenly started to release new projects and suppliers picked up on the quoting activity from the third quarter. This trend seems to be set to continue and the start of the new year has been surprisingly busy.”