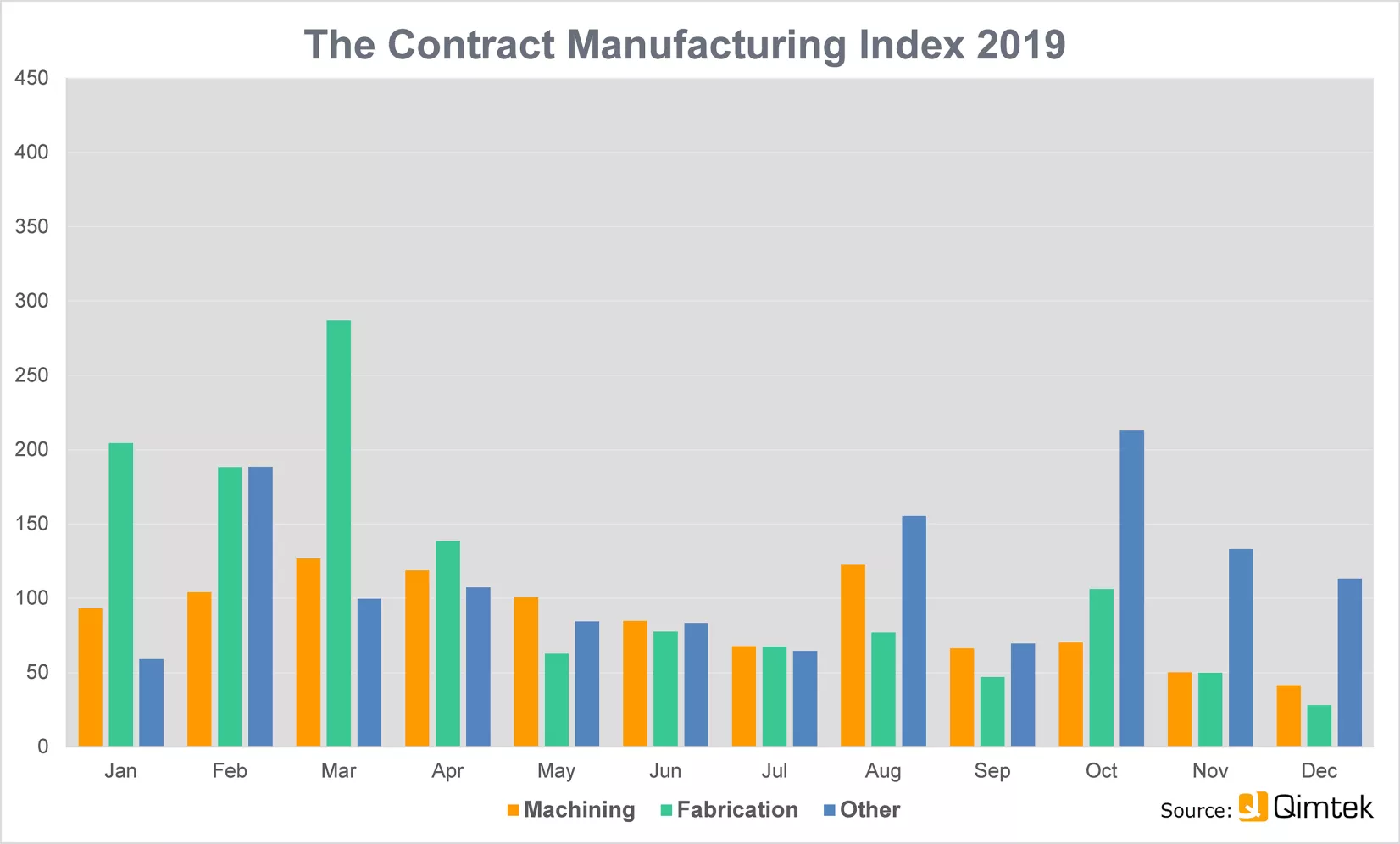

The Contract Manufacturing Index (CMI) for the final quarter of 2019 showed a further deterioration in the UK subcontract manufacturing market. It fell 23% from what had already been a poor third quarter. Overall the market was 56% down on the final quarter of the previous year.

The index was it its lowest levels since it was first published, falling to 66 compared to the baseline figure of 100 which represents the average value of the subcontract market between 2014 and 2018.

The biggest change over the quarter was in fabrication, which had previously been one of the strongest performers but fell 36%. Machining, in comparison, fell by a relatively modest 15% and other processes, such as electronics and moulding, actually saw a slight rise.

Fabrication still accounted for 41% of the market though, with machining on 38% and other processes accounting for the remainder.

Heavy and construction vehicles were by far the strongest performers in the final quarter – reaching levels over 17 times higher than at the start of the year. Other sectors that were up on the previous quarter included consumer products and industrial machinery.

Looking at the year as a whole, the strongest markets were heavier industries such as energy, oil, chemical, construction and construction vehicles, with scientific equipment also coming in the top four and defence in fifth place.

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies who could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

Commenting on the figures, Qimtek owner Karl Wigart said: “It was a disappointing end to a disappointing year. An early rally in February and March looked promising but was just a brief uptick on what proved to be a consistent downward trend.

“The latter part of the year was a period of particular uncertainty for manufacturing and that was reflected in the Index. Whether the recent election and fixed date for Brexit will reverse that trend remains to be seen.

“Looking at the last quarter, there was a small uplift in October which was probably a bit of stockpiling before the second Brexit deadline but then it dropped again.

“December showed a bit of a slowdown, but not much more than is usual for the year end. Hopefully, 2020 will see a recovery in manufacturing activity.”