Karl has been involved in the business to business information service since 1990. Having spent time with information to the construction and manufacturing industry in the UK, Sweden, Switzerland, Germany and the US.

The Contract Manufacturing Index (CMI) has been developed to reflect the total purchasing budget of companies that are looking to outsource manufacturing in any given month.

This reflects a sample of over 4,000 companies, who have a purchasing budget of more than £3bn and a supplier base sample of over 7,000 vendors, with a verified turnover in excess of £25bn.

We measure this by extracting data from the projects we receive from manufacturing purchasers who have an active need for the services of subcontract engineering suppliers.

Since 2016, we have published the index quarterly and the following is a summary of our findings for the second quarter of 2018. In order to shed more light on the emerging trends, we have also broken this down by process and industry.

Key Points

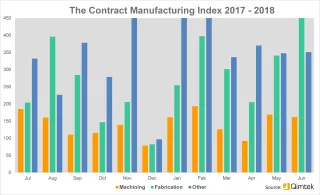

- The Index is split into three processes - Machining, Fabrication, and Others.

- 2018’s data for quarter 2 is collected from 349 companies and 526 projects.

- Quarter 2’s results are down 5% from the previous quarter and up 30% on the comparable quarter for 2017

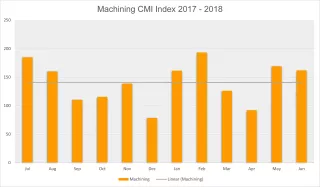

Machining

The machining index started to regain traction in quarter 1, having risen by 31%. However, quarter 2 saw it fall by a total of 12%, meaning that some - but not a majority - of quarter 1’s growth has now tailed off. With 2017 proving to be an extremely fruitious year for the index at large, it’s perhaps not a surprise to see that 2018’s Q2 results are 5% down on the comparable quarter for 2017.

- 45% of the second quarter’s projects were for machining processes.

- The buyers who gave us these projects have a total outsourcing value of £21,877,603.

- Quarter 2’s machining index fell by 12% on the preceding quarter and was down by 5% in comparison to the second quarter of 2017.

Fabrication

2018 has certainly proved to be a positive year for the fabrication index thus far, with quarter 2’s results continuing the precedent of growth set by quarter 1. The latest results show a further 5% rise on top of the dramatic 54% growth experienced between January and March; further still, the 2018 index for quarter 2 has expanded by 70% against the respective quarter last year. In fact, 44% of all projects generated within quarter 2 were for fabrication processes, which brings it up to only 1% less than machining.

- 44% of the second quarter’s projects were for fabrication processes.

- The buyers who gave us these projects have a total outsourcing value of £35,059,517.

- The fabrication index grew by 5% in comparison to quarter 1, with the latest results showing a massive 70% rise against 2017’s quarter 2 index.

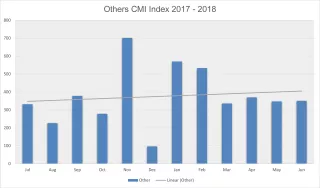

Others

Representing processes such as casting, toolmaking, finishing, plastics & rubber, the ‘Others’ category only makes up 11% of the projects from the second quarter and is therefore more difficult to monitor. However, quarter 2’s results do not bode well for this category, uncovering a 26% decrease against quarter 1’s 25% growth. Therefore, this index is now back to performing just slightly under where it was at the turn of the year, although it is still 20% bigger than Q2 2017.

- 11% of the second quarter’s projects were for processes that fall under the ‘Others’ category.

- The buyers who gave us these projects have a total outsourcing value of £5,344,833.

- The index for these processes grew by 20% compared to the second quarter of 2017.

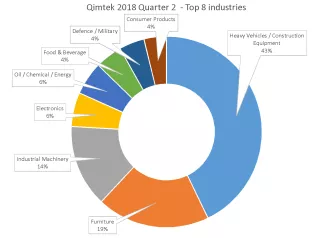

Industry

- Heavy vehicles/construction equipment remains top of the leaderboard for the second quarter running, representing a sizeable 43% of the market.

- The furniture industry increased their outsourcing dramatically during Quarter 2, rising all the way from fourteenth place into second.

- Industrial machinery retained its standing in third place, accounting for 14% of the market across both quarter 1 and quarter 2.

Quarter 2’s results report the same first and third top industries as quarter 1. Heavy vehicles/construction equipment continued to dominate the top spot over the last three months and has gone from representing 23% of the market to a remarkable 43%. Industrial machinery has been static in comparison, making up 14% of the market across the whole of 2018 to date; however, this has allowed it to remain in third position over both quarters.

The previous quarter’s runner-up - the automotive sector - did not fare so well from April to June, dropping all the way down into ninth position and out of the top industries altogether. Taking its place, the furniture industry has rapidly ascended from fourteenth place into second, making it the most active industry in terms of sheer growth.

That’s not to say that furniture is the only industry to increase their outsourcing during quarter two. Although consumer products accounts for just 4% of the market, it has risen into fourth place from sixteenth; likewise, the defence sector featured in eighteenth place during quarter 1 and has now climbed into seventh.

Summary

The figures for 2018’s second quarter are very encouraging, especially given the comparative 30% growth to its 2017 equivalent.

The main driver behind this growth is the fabrication index, which has experienced a period of steady expansion since the first quarter of 2016. Within the same time frame, the machining index has remained somewhat level - an observation that is supported by the latest results, with machining only experiencing a 5% rise to the fabrication index’s 70%.

The last three months have also witnessed a shake-up in the top industries represented by the market, with the automotive sector undergoing a significant decrease in outsourced manufacturing, countered by the gathering buoyancy of the furniture, defence and consumer products industries. The latter sectors have re-emerged within the results after experiencing a drop-off in quarter 1.

After receiving repeat feedback that many manufacturers are choosing to invest in machinery to bring production in-house, we are as of yet unsure as to how this will affect the index over the coming months. However, with the fabrication industry going from strength to strength and machining experiencing less pronounced growth, this has certainly not been reflected in the index thus far.