Karl has been involved in the business to business information service since 1990. Having spent time with information to the construction and manufacturing industry in the UK, Sweden, Switzerland, Germany and the US.

- The Index is split into three processes - Machining, Fabrication, and Others.

- 2021’s data for Quarter 2 is collected from 243 companies and 407 projects.

- Quarter 2 2021's Index shows a slump of 8% against the preceding quarter; however, it was 57% larger than the comparable quarter for 2020.

- Both April and May reported fairly low levels of outsourcing, although activity surged across all three indexes within June - most notably the Machining Index. This serves as a positive omen to Quarter 3's output.

- The number of projects awarded has grown steadily over the course of 2021 and Quarter 2 is no exception - June had the highest number of awarded projects within the last 12 months, meaning that the average order value has remained high.

The Contract Manufacturing Index for the second quarter of 2021 brings with it a slowdown in outsourcing activity. The overall value of the Index fell by 8% from April to June, with the Fabrication Index and Others Index showing a pronounced decline from the first quarter of the year. These indexes fell by 25% and 22% respectively; meanwhile, the Machining Index bucked this trend and grew by an astronomical 120%, with significant impetus attributed to its strong performance during June 2021.

June exhibited much higher levels of outsourcing across all three indexes.

This increase in activity towards the end of the quarter was consistent across all three indexes. Whilst April and May proved challenging for the subcontract manufacturing industry as a whole, June exhibited much higher levels of outsourcing. This indicates that we can perhaps begin to look forward to a more positive third quarter in terms of output.

Both the Machining Index and the Fabrication Index also recorded growth against the comparable quarter of 2020; however, this is unsurprising given that the UK was in the midst of its first national lockdown throughout most of this time period. What is perhaps more surprising is the performance of the Others Index by comparison - as the only outlier to the aforementioned observation, this index has plummeted 48% against the second quarter of 2020.

Despite a decline within the total amount of outsourcing, the average order value has remained high.

Despite a decline within the total amount of outsourcing during this period, it's interesting to note that the average order value has remained high. This gives credence to an emerging trend concerning the number of projects being awarded - as these figures have climbed steadily over the course of the year so far, it seems that buyers are now in a position to push the button on their subcontract requirements, with less speculative enquiries overall.

The slump reflected in the latest results could be attributed to the global materials shortage, which is currently interfering with the efforts of manufacturing buyers and subcontract engineering suppliers alike. However, an uptick in activity across all three indexes within June hints that the industry can expect better results within the third quarter of the year - indeed, the Index's trajectory seemed to have taken a turn for the better as the quarter drew to a close.

Machining

The Machining Index has not fared well against the backdrop of the COVID-19 pandemic; however, Quarter 2's results indicate that some significant recuperation could be underway. Whilst April and May recorded low levels of outsourced machining, June saw a massive increase in activity that positively impacted the overall results for the entirety of the quarter. In comparison to the preceding quarter, the Machining Index grew by 120% with a total outsourcing value of £14,658,698 - furthermore, this value was 26% higher than the second quarter of 2020.

- 53% of the first quarter’s projects were for machining processes.

- The buyers who gave us these projects have a total outsourcing value of £14,658,698, compared to a value of £10,635,447 in Quarter 1 2021.

- This Index has displayed growth of 120% in comparison to Quarter 1 and 26% against Quarter 2 2020.

Fabrication

The Fabrication Index did not experience the same good fortune as that of the Machining Index during Quarter 2, finishing 25% behind the preceding quarter. Despite a strong start to the year, outsourced fabrication activity levels fell dramatically from March to May, which hampered the overall results for the second quarter. However, June saw the Fabrication Index rise to levels comparable to the start of the year, which serves as an encouraging prelude to the start of the third quarter.

Despite a disappointing result within the context of the year so far, it's important to note that the latest Fabrication Index is still 75% higher than the comparative quarter for 2020 - a period during which the UK entered its first national lockdown.

- 40% of the first quarter’s projects were for fabrication processes.

- The buyers who gave us these projects have a total outsourcing value of £15,561,755, compared to £20,624,453 during Quarter 1 2021.

- The Fabrication Index finished 25% down on the previous quarter, but still displayed 75% growth in comparison to the second quarter of 2020.

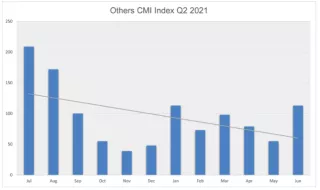

Others

Representing processes such as casting, toolmaking, finishing, plastics & rubber, the ‘Others’ category makes up 7% of the projects generated within the second quarter and is therefore more difficult to monitor. The second quarter brought with it a sizeable decline to this particular index, which shrank by 22% in relation to Quarter 1. In addition, it is the only index to report a decline in comparison to the second quarter of 2020 - at 48%, this drop in activity is also very pronounced. Nonetheless, the Others Index did see an increase in activity within June, which could pave the way for a more positive trajectory within the next quarter.

- 7% of the first quarter’s projects were for processes that fall under the ‘Others’ category.

- The buyers who gave us these projects have a total outsourcing value of £2,891,475, compared to a value of £3,680,053 in Quarter 1, 2021.

- This latest result is 22% down on the previous quarter; furthermore, it is also 48% less than the second quarter of 2020.

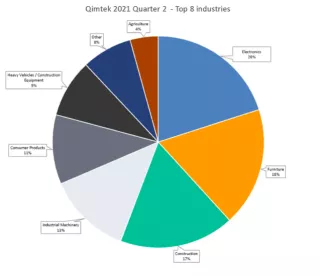

Industry

- The Electronics industry had the highest levels of outsourcing during Quarter 2, 2021, rising from third place into first place with a 20% share of all outsourcing activity from April to June.

- The Furniture sector maintained its position in second place for the second consecutive quarter, accounting for 18% of all outsourcing within Quarter 2.

- The Construction sector experienced a surge in activity within Quarter 2, ascending from fifth place into third. This industry finished just behind the Furniture sector, contributing 17% of the total spend on subcontract manufacturing during this period.

- The industry leader for Quarter 1, Industrial Machinery, sank into fourth place amidst a decline in outsourcing levels.

There have been a number of changes this quarter to the top industries represented within the Contract Manufacturing Index. At the top of the leaderboard, the Electronics industry usurped the efforts of all other sectors as the top contributor towards outsourced manufacturing from April to June. Representing 20% of all spending within this period, the Electronics industry rose from its previous position in third place to knock Quarter 1's leader, Industrial Machinery, off of the top spot, with the latter descending into fourth place amidst a decline in outsourcing levels.

For the second consecutive quarter, the Furniture industry has maintained its grasp on second place, contributing 18% of the total outsourcing spend within Quarter 2. The Construction sector placed marginally behind with a 17% share, finishing the quarter third overall and rising from fifth place in Quarter 1.

There have been a number of newcomers to the latest results. The Consumer Products industry made its first appearance since the fourth quarter of 2019, featuring in fifth place for Quarter 2 and accounting for 11% of the total spend. Meanwhile, the Heavy Vehicles/Construction Equipment industry came in sixth place with a 9% share, having fallen out of the running altogether from the final quarter of 2020 into the first quarter of 2021. The Agriculture sector also appeared in the top industries for the first time in a year as the eighth biggest spender on subcontract services from April to June.

Another notable consistency from Quarter 1 into Quarter 2 is the grasp that 'Other' industries - that is, industries that fall outside of Qimtek's specified sectors - maintained on seventh place.

The abundance of newcomer industries to Quarter 2's results also shows us that outsourcing declined amongst a number of sectors - namely Communication Equipment, Environmental Technology and Medical/Scientific, which did not place within the top industries during the second quarter of 2021.

About the Contract Manufacturing Index

The Contract Manufacturing Index (CMI) has been developed to reflect the total purchasing budget of companies that are looking to outsource manufacturing in any given month.

This reflects a sample of over 4,000 companies, who have a purchasing budget of more than £3bn and a supplier base sample of over 7,000 vendors, with a verified turnover in excess of £25bn.

We measure this by extracting data from the projects we receive from manufacturing purchasers who have an active need for the services of subcontract engineering suppliers.

Since 2016, we have published the index quarterly and this report is a summary of our findings for the second quarter of 2021. In order to shed more light on the emerging trends, we have also broken this down by process and industry.