Karl has been involved in the business to business information service since 1990. Having spent time with information to the construction and manufacturing industry in the UK, Sweden, Switzerland, Germany and the US.

- The Index is split into three processes - Machining, Fabrication, and Others.

- 2025’s data for Quarter 3 is collected from 216 companies and 313 projects.

- Quarter 3's Index increased by 10% against the preceding quarter.

On the face of it, the index looked very strong, and it was, for July and August. However, September was very slow. There was good activity both from buyers and Suppliers in the two first months but in the last it slowed down drastically from both. What is a bit surprising, is that quoting activity has dropped as well as lead times. When the manufacturing sector is slow, you would expect a highly competitive quoting for custom made parts but that is not the case. Are suppliers of custom made parts cautious and not trying to grow as it is difficult and expensive to employ more staff?

Machining

- 53% of third quarter projects were from machining processes.

- The buyers of machining processes have a total outsourcing value of £19,191,650

- The index for machining is slightly down 2% from previous quarter and up 68% on previous year

Although the overall Contract Manufacturing Index (CMI) appeared very strong, this was largely driven by July and August. The activity from both buyers and suppliers slowed down drastically in September.

Fabrication

- 36% of second third projects were from fabrication process

- The buyers of fabrication processes has a total outsourcing value of £25,780,700

- The index for Fabrication is up 18% on last quarter and 140% up on last year's figures

Very much the same story as Machining, very robust in July and August but then slowed down in September.

Other

- 11% of third quarter projects were from other processes

- The buyers of other processes has a total outsourcing value of £3,620,383

- The index for Others is up 45% on last quarter and more than 200% of last year's third quarter.

The "Others" process category, which captures processes outside of Machining and Fabrication, saw the strongest growth compared to the previous year, although it represented the smallest share of total projects

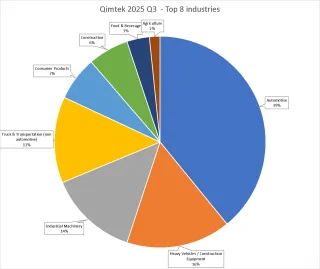

Industry

The Contract Manufacturing Index (CMI) industry data for Q3 2025 reveals significant shifts in outsourcing budgets among the top eight sectors compared to Q2 2025, although the Automotive sector maintained the Rank 1 position in both quarters, a feat noted in Q2 as being mainly due to the inclusion of very large Tier 1 manufacturers.

The most dramatic increases in outsourcing activity were concentrated in heavy industry and transportation: Heavy Vehicles / Construction Equipment climbed from Rank 5 in Q2 to Rank 2 in Q3, Truck & Transportation (non automotive) jumped substantially from Rank 12 to Rank 4, and Construction rose from Rank 10 to Rank 6.

Furthermore, the Agriculture sector experienced a major surge in ranking, moving from Rank 17 in Q2 to Rank 8 in Q3. Industrial Machinery remained consistently strong, holding Rank 3 across both quarters, though Q2 commentary noted this was a drop from its usual first-place standing. Rounding out the top eight, Consumer Products experienced a slight dip from Rank 4 to Rank 5, while Food & Beverage maintained a steady position at Rank 7

Lead times

The Contract Manufacturing Index (CMI) lead times showed a reduction throughout Quarter 3 (Q3) of 2025, which was noted as a surprising trend. In July, the average lead time was 21 days, which then dropped to 17 days in August, before slightly increasing to 19 days in September.

The reduction in lead times during Q3 occurred concurrently with a decrease in quoting activity. This specific dynamic—where both quoting activity and lead times dropped—was unexpected, as a slow manufacturing sector would typically result in highly competitive quoting for custom-made parts.

Contextually, this Q3 movement contrasts with the end of Quarter 2 (Q2), where lead times had dropped to 19 days in April and May but then jumped up to 22 days in June. Similarly, in Quarter 1 (Q1), lead times dropped during the most active quoting months (January and February) but went up when overall activity dropped off in March

About Contract Manufacturing Index

The Contract Manufacturing Index (CMI) has been developed to reflect the total purchasing budget of companies that are looking to outsource subcontract manufacturing of custom made parts in any given month.

This reflects a sample of over 4,000 companies, who have a purchasing budget of more than £5bn and a supplier base sample of over 7,000 vendors, with a verified turnover in excess of £25bn.

We measure this by extracting data from the projects we receive from manufacturing purchasers who have an active need for the services of subcontract engineering suppliers.

Since 2016, we have published the index quarterly and this report is a summary of our findings for the this current quarter. In order to shed more light on the emerging trends, we have also broken this down by process and industry.