Karl has been involved in the business to business information service since 1990. Having spent time with information to the construction and manufacturing industry in the UK, Sweden, Switzerland, Germany and the US.

The Contract Manufacturing Index (CMI) has been developed to reflect the total purchasing budget of companies that are looking to outsource manufacturing in any given month.

This reflects a sample of over 4,000 companies, who have a purchasing budget of more than £3bn and a supplier base sample of over 7,000 vendors, with a verified turnover in excess of £25bn.

We measure this by extracting data from the projects we receive from manufacturing purchasers who have an active need for the services of subcontract engineering suppliers.

Since 2016, we have published the index quarterly and the following is a summary of our findings for the fourth quarter of 2018. In order to shed more light on the emerging trends, we have also broken this down by process and industry.

Key points:

- The Index is split into three processes - Machining, Fabrication, and Others.

- 2018’s data for Quarter 4 is collected from 285 companies and 399 projects.

- Quarter 4’s results have reported no significant changes compared to Quarter 3 2018, but are up more than 60% on the comparable quarter for 2017.

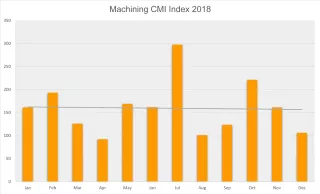

Machining

Quarter 3 saw the machining index grow by 23%; however, Quarter 4’s results did not follow the same trajectory and fell by 6% in comparison. This is due to a month-to-month decline from October to December, despite the index getting off to a strong start. Nonetheless, 2018’s Quarter 4 machining index is up by a massive 47% compared to the last quarter of 2017, whilst machining processes accounted for 45% of all projects generated.

- 45% of the fourth quarter’s projects were for machining processes.

- The buyers who gave us these projects have a total outsourcing value of £25,257,333, which falls in line with the average for the year.

- Quarter 4’s machining index fell by 6% in comparison to the preceding quarter, but grew by 47% from the comparable quarter for 2017.

Fabrication

Much like the machining index, Quarter 4’s fabrication index reported a downfall of 4% in comparison to the preceding quarter. It showed a marked deficit in December after above-average results throughout October and November, though the index declined consistently over the course of the last three months. This defies the trend set by Quarter 3, during which the index showed gradual growth after a dramatic drop in July. Overall, 42% of the fourth quarter’s projects were comprised of fabrication processes; nonetheless, these results were up by a sizeable 68% on the comparable quarter for 2017.

- 42% of the fourth quarter’s projects were for fabrication processes.

- The buyers who gave us these projects have a total outsourcing value of £25,487,187, which is below average for the year.

- The fabrication index fell by 4% in comparison to 2018’s third quarter, although the latest results reported growth of 68% in comparison to Quarter 4 2017’s index.

Other

Representing processes such as casting, toolmaking, finishing, plastics & rubber, the ‘Others’ category makes up 13% of the projects from the fourth quarter and is therefore more difficult to monitor. In spite of this, the results for Quarter 4 are up 34% on the third quarter, during which only 8% of projects generated were for processes that fell under the ‘Others’ umbrella. This is extremely encouraging, with the index having now shown pronounced growth throughout the entirety of the second half of 2018.

- 13% of the fourth quarter’s projects were for processes that fall under the ‘Others’ category.

- The buyers who gave us these projects have a total outsourcing value of £10,451,500 - an increase on the average for the year.

- The index for these processes grew by 34% compared to the third quarter, which confirms consistent and pronounced growth throughout the entirety of the latter half of 2018.

Industry

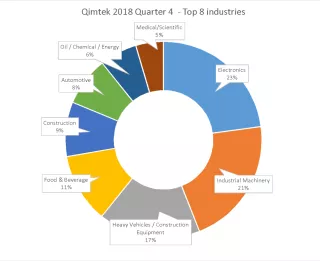

The electronics industry has gone from strength to strength, with Quarter 4’s results putting it at the top of the table with a 23% hold on the market.

The industrial machinery sector has seen a resurgence during Quarter 4 after a disappointing third quarter, seeing it rise to second place with a 21% standing.

The heavy vehicles/construction equipment industry has also regained some of the ground it lost during Quarter 3, as it re-emerges into the top industries with a 17% share of the market.

The automotive and furniture industries suffered a vast decrease in outsourcing and have subsequently forfeited first and second place respectively within Quarter 4.

There is little consistency between the standing of individual industries reported from Quarter 3 to Quarter 4. The only sector to retain representation in the top three industries over the entirety of 2018’s third and fourth quarters is electronics, which has seen a rise in manufacturing outsourcing and places first within the latest results. In fact, 23% of the market is now represented by electronics, compared to 13% in Quarter 3.

Whilst the automotive and furniture sectors enjoyed a high-output third quarter, both of these industries have fallen from the top of the table during Quarter 4. Automotive - being the forerunner from July to September - is now in sixth place, with a market share of just 8% in comparison to the 19% it previously held. The furniture sector has also scaled back outsourcing levels drastically, taking it from second place in Quarter 3 to eleventh in Quarter 4.

This shake-up has made way for both the industrial machinery and heavy vehicles/construction equipment sectors to climb the ranks, with these industries now occupying second and third place respectively. Industrial machinery previously held fifth place with 12% of the market; however, this has increased to 21% from October to December. The heavy vehicles/construction equipment industry has reported recuperation and as a result, it has risen into third place.

Food & beverage has remained somewhat static, with only 1% growth from Quarter 3 to Quarter 4, although its position in the table has improved to fourth place due to a slowdown reported by other industries. The medical/scientific sector - having previously placed fourth - has seen its contribution towards outsourced manufacturing decline to 5%, putting it in eighth place during 2018’s final quarter.

Meanwhile, the oil/chemical/energy industry has reappeared in the top sectors represented, coming in seventh place.

Summary

Unfortunately for Quarter 4’s index, the growth of October and November was sabotaged by an extremely slow December, meaning that two out of the three sub-indexes reported an overall decline in outsourced manufacturing. The most pronounced case of this lies within the fabrication index, which experienced its worst month of the year in December. Although October and November’s results for this sub-index were stronger than any seen in Quarter 3, December’s plummet was so pronounced that it brought down the index as a whole, resulting in a 4% decrease from quarter to quarter.

The ‘Others’ index, however, experienced rapid growth of 34% from Quarter 3 to Quarter 4, showing that niche processes are rising in popularity amongst manufacturing buyers. This growth could also result from the decline in both machining and fabrication, as it now accounts for a larger percentage of the projects generated overall.

The electronics industry has increased its contribution towards the purchase of subcontract engineering services, whilst the automotive and furniture sectors have scaled back their spending in these areas. This has made way for both the industrial machinery and heavy vehicles/construction equipment industries to take over in second and third place.

Whilst we can speculate that December’s drop in outsourced manufacturing is largely a seasonal trend, it cannot yet be claimed with certainty that a downturn will not preside over the months that follow. However, the overall good health of October and November’s outsourced engineering output is a positive omen that the industry will regain traction in early 2019.