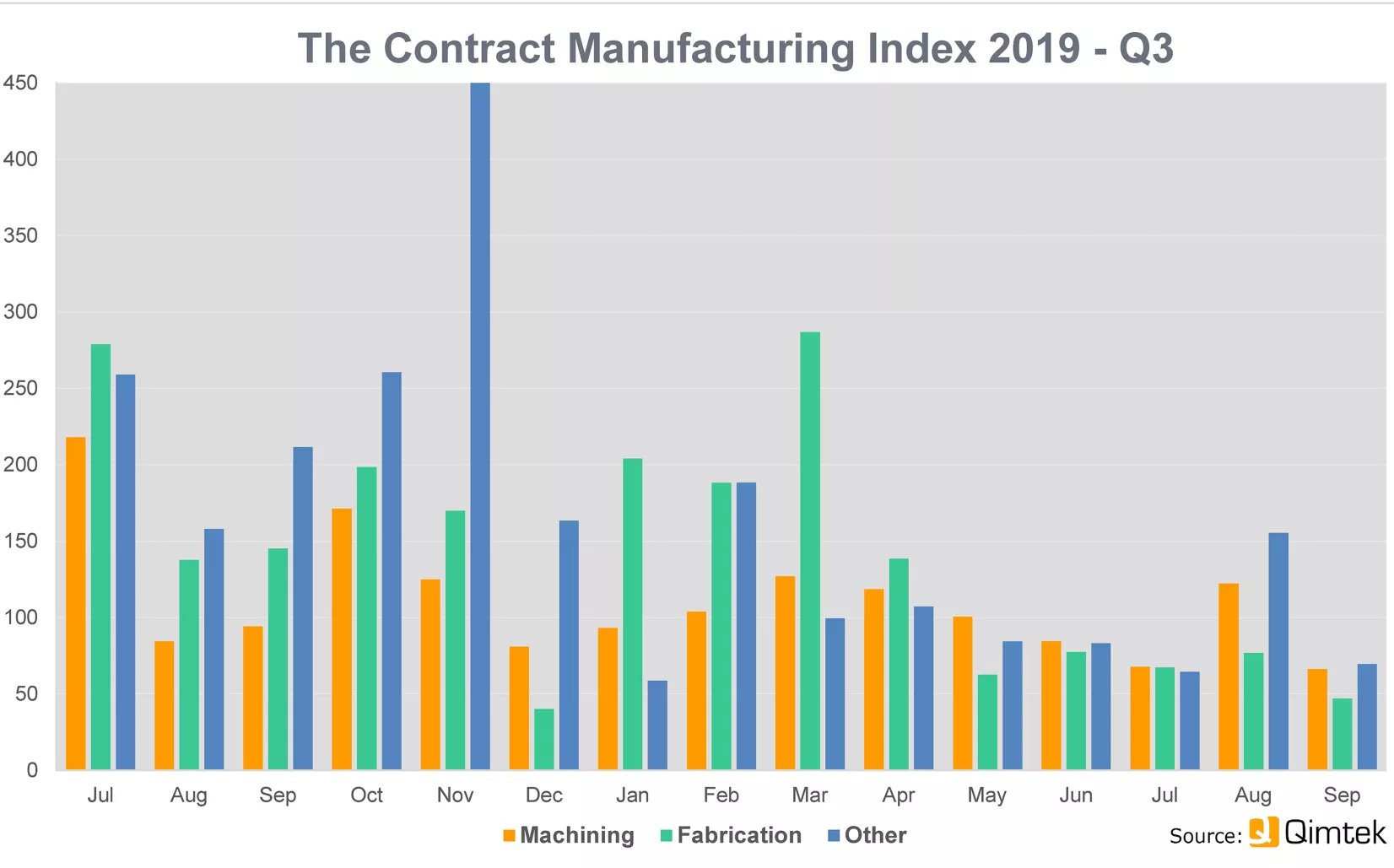

The subcontract manufacturing market fell by 15% in the third quarter of 2019 and is down 47% year-on-year according to the latest Contract Manufacturing Index (CMI).

The overall number of projects is at quite a high level, but these are mainly from smaller companies and the large OEMs are not putting out any new work.

Machining has seen the biggest drop, down over 30% on the previous quarter, while fabrication is actually up by 5%.

Machining now accounts for 35% of the value of the market, with fabrication at 50% and other processes, such as moulding and contract electronic manufacturing, accounting for the remaining 15%.

The biggest sectors in the index were the biggest fallers, with construction, construction machinery and electronics dropping significantly. There were some encouraging trends though, with medical equipment, automotive and oil and gas increasing – one surprising growth area was in furniture manufacture, which was up by 144%.

Compared to the third quarter of 2018, the market has dropped by almost half (47%), despite a relatively strong performance in the first quarter of this year.

It is now 30% lower than when the EU referendum was held in 2016.

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies who could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

Commenting on the figure, Qimtek owner Karl Wigart said: “Until April the market had been fairly steady but it has seen a significant decline since then.

“We are hearing from the market around the UK that uncertainty over the outcome and impact of Brexit is certainly a factor and there is a fair degree of spare capacity waiting for new projects.

“There are actually more projects out to tender than there have been all year, but it is small companies that are looking to outsource rather than the larger OEMS. This suggests that the OEMs are looking for clarity before making strategic decisions, whereas for the smaller, more nimble, companies it is more or less business as usual.”