Karl has been involved in the business to business information service since 1990. Having spent time with information to the construction and manufacturing industry in the UK, Sweden, Switzerland, Germany and the US.

- The Index is split into three processes - Machining, Fabrication, and Others.

- 2021’s data for Quarter 3 is collected from 229 companies and 389 projects.

- The latest Index shows growth of 52% against the preceding quarter; however, it was 5% smaller than the comparable quarter for 2020.

- Both July and August exhibited substantial activity, although levels slowed down towards the end of the quarter.

- A shortage in materials, staff and transport has meant that the average number of quotes received per project has fallen dramatically, dropping below the eight-year average of 2.8.

The third quarter of 2021 started on an overwhelmingly positive note, with comparisons to be drawn with the results for quarter 1. July and August were largely buoyant across all three indexes, with significant outsourcing activity taking place across the board. However, September put a dampener on the overall value as levels plummeted within the Fabrication and Others Index, although it is interesting to note that the Machining Index actually bucked the trend and began ascending during the final month of the quarter.

This downturn in activity can be largely attributed to a lack of resources such as materials, transport and staff.

This downturn in activity can be largely attributed to a lack of resources such as materials, transport and staff. The worldwide materials shortage continues to create problems within the supply chain, meaning that many subcontract suppliers are unable to fulfil orders and are therefore hesitant to commit to undertaking new projects.

With so much uncertainty presiding over availability of resources, the average number of quotes received per project fell dramatically from July to September. Many projects have gone unquoted altogether, whilst the average number of quotes per project for quarter 3 fell below the eight-year average of 2.8. This illustrates perfectly that although subcontract work is there for the taking, the bottleneck lies very much with the resources available to suppliers at any given time.

These issues are likely to remain as long as the materials shortage continues, with a lack of available fuel further compounding this unfortunate situation. This means that as we move into the final quarter of the year, the trajectory of the Index is likely to continue down a similar path; however, we remain optimistic that the new year will bring relief to the industry as it continues to strive to meet demand.

READ: Contract Manufacturing index - Quarter 2, 2021

Machining:

The Machining Index continued its upwards trajectory from July to September.

After some significant recuperation during the second quarter of 2021, the Machining Index continued its upwards trajectory from July to September. With growth of 120% from quarter 1 to quarter 2, the latest results reinforce this trend with a further 22% increase, solidifying the subcontract machining market's recovery following the COVID-19 pandemic.

Furthermore, the Machining Index also grew in comparison to 2020, finishing 10% up on the third quarter of 2020. While July proved to be the strongest month for the Index before a slight drop in August, September's results showed a clear upwards trend that should hopefully preside as we move into the final quarter of the year.

- 52% of the third quarter’s projects were for machining processes.

- The buyers who gave us these projects have a total outsourcing value of £17,866,572, compared to a value of £14,658,698 in Quarter 2 2021.

- This means that the Machining Index finished 22% up on the previous quarter and 10% larger than the third quarter of 2020.

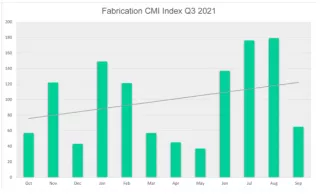

Fabrication:

The Fabrication Index experienced a dramatic drop in activity during September.

The Fabrication Index was much more erratic than the Machining Index in terms of its output. Although the overall result for the third quarter was overwhelmingly positive, displaying growth of 71% in comparison to the preceding quarter, the Fabrication Index experienced a dramatic drop in activity during September. With the results for July and August being the strongest of the year so far, the end of the quarter was disappointing in terms of output - furthermore, this was reflected in the comparisons to 2020, with a 12% drop against the corresponding quarter.

- 40% of the third quarter’s projects were for fabrication processes.

- The buyers who gave us these projects have a total outsourcing value of £26,420,655, compared to £15,561,755 during Quarter 2 2021.

- The Fabrication Index grew by 71% from the previous quarter, but finished 12% down on the comparable quarter for 2020.

READ: Contract Manufacturing Index - Quarter 1, 2021

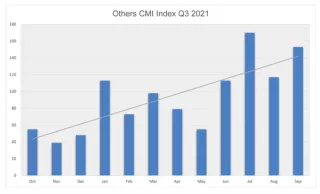

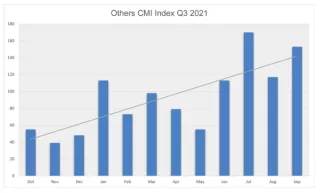

Others:

The Others Index underwent an extremely positive third quarter, with prominent growth of 99% from quarter 2 to quarter 3.

Representing processes such as casting, toolmaking, finishing, plastics & rubber, the ‘Others’ category makes up 8% of the projects generated within the third quarter and is therefore more difficult to monitor. With that being said, the Others Index underwent an extremely positive third quarter, with prominent growth of 99% from quarter 2 to quarter 3. Much like the Machining Index, the Others Index saw its strongest performance take place during July, before a slight dip in August and recovery during September. Nonetheless, this result was not enough for the Index to grow in comparison to the previous year, with a 6% drop against the third quarter of 2020.

- 8% of the third quarter’s projects were for processes that fall under the ‘Others’ category.

- The buyers who gave us these projects have a total outsourcing value of £5,701,900, compared to a value of £2,891,475 in Quarter 2, 2021.

- This latest result is up by an astronomical 99% on the previous quarter, but still down 6% compared to the third quarter of 2020.

Industry:

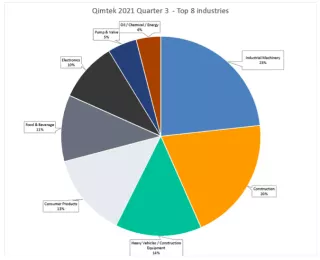

- Having previously placed fourth, the Industrial Machinery sector emerged as the top purchaser of subcontract engineering services from July to September, accounting for 23% of spending during this period.

- Meanwhile, the Construction industry also had a small boost in activity, rising from third place into second with a 20% share of the total spend.

- The Heavy Vehicles/Construction Equipment industry rose from sixth place into third during quarter 3, with a 14% share of all subcontract purchasing.

- Quarter 2's forerunner, the Electronics sector, slowed down its outsourcing activity significantly and finished the third quarter in sixth place.

The third quarter of 2021 saw a lot of movement within the top industries represented by the data.

The third quarter of 2021 saw a lot of movement within the top industries represented by the data. Having finished the second quarter in fourth place, the Industrial Machinery sector soared to the top of the leaderboard in quarter 3, accounting for 23% of all subcontract engineering purchases during this period. Meanwhile, the Construction industry also ascended into second place, after finishing third during quarter 2. With a 20% share of all subcontract spending from July to September, Construction was not far behind the quarter's leader in terms of activity. However, a larger gap emerged between second and third place, with the Heavy Vehicles/Construction Equipment sector holding a 14% share of this quarter's overall spend.

Further down the results, quarter 3 proved to be a buoyant period for the Consumer Products industry, which finished in fourth place and accounted for 13% of subcontract purchasing - only a fraction behind that of the Heavy Vehicles/Construction Equipment sector. Food & Beverage appeared in fifth place with 11%, making this the sector's first appearance in the top industries since the third quarter of 2020. Sixth position was held by the Electronics industry - having been the forerunner of quarter 2's results, Electronics seems to have undergone a lull in subcontract purchasing activity, accounting for only 10% of subcontract spending from July to September 2021.

Elsewhere the Pump & Valve sector reappeared in quarter 3's results, having dropped out of the results altogether since the second quarter of 2020. Oil/Chemical/Energy was another newcomer to the latest results, having also been absent since quarter 3 2020. This industry held a 4% share of the overall spend, finishing in eighth place.

Meanwhile, a number of industries fell out of the running entirely moving from quarter 2 into quarter 3, including Furniture (previously second), Other (previously seventh) and Agriculture (previously eighth).

About the Contract Manufacturing Index

The Contract Manufacturing Index (CMI) has been developed to reflect the total purchasing budget of companies that are looking to outsource manufacturing in any given month.

This reflects a sample of over 4,000 companies, who have a purchasing budget of more than £3bn and a supplier base sample of over 7,000 vendors, with a verified turnover in excess of £25bn.

We measure this by extracting data from the projects we receive from manufacturing purchasers who have an active need for the services of subcontract engineering suppliers.

Since 2016, we have published the index quarterly and this report is a summary of our findings for the third quarter of 2021. In order to shed more light on the emerging trends, we have also broken this down by process and industry.